Empower and Quicken are two popular personal finance apps for budgeting, investment tracking, and retirement planning. Both platforms can help you achieve savings goals, track spending, and visualize your financial future.

However, multiple differences make one product a better option for your needs. I have used both services over the years and will help you compare the best features with this Quicken vs. Empower comparison.

What is Empower?

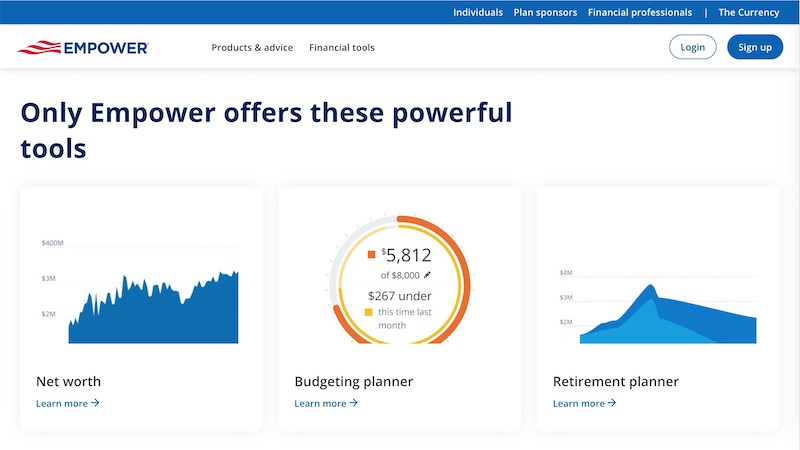

Empower, previously known as Personal Capital, is a free retirement app with a net worth tracker, basic budgets, and investment portfolio analyzers. It also offers optional wealth management services for portfolios with a minimum value of $100,000.

Notable free financial tools worth highlighting include:

- Budgeting planner

- Cash flow (monthly income vs. expenses)

- Net worth tracker

- Retirement planner

- Savings planner

- Investment tracking

- Investment portfolio analyzer

I use this platform for its free net worth tracking and retirement planner. It’s one of the most impressive free budgeting apps, as it syncs to your financial accounts and lets you add manual accounts to track your spending and make custom savings goals easily.

While there’s plenty to like about Empower, its budgeting tools are somewhat limited as the platform is primarily for those who already live within their means and are ready to focus on increasing their net worth.

What is Quicken?

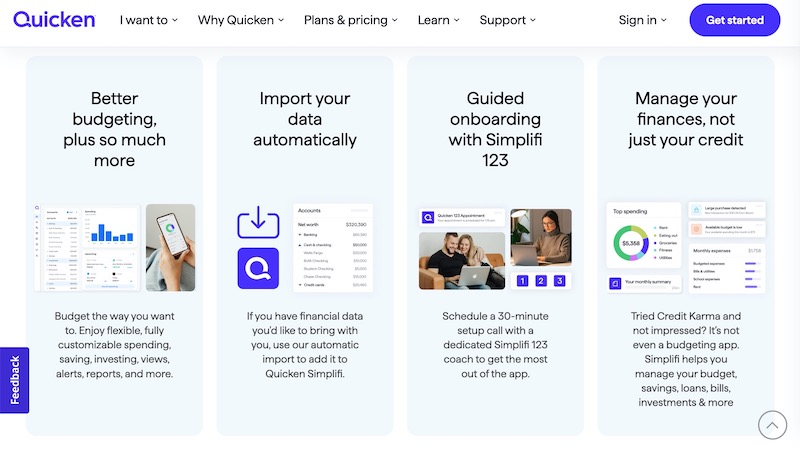

Quicken is a paid budgeting app offering several plans with incrementally more features. You can also download desktop software and access more budgeting features than Empower offers.

Simplifi by Quicken is the most affordable option and the best fit for most people with its versatile budgeting features. Consider it instead of Empower to make a detailed budget while having good investment tracking and financing planning tools.

Its core features include:

- Customizable spending plan

- “Safe to spend” calculations based on actual spending

- Bill payment reminders

- Investment tracker

- Financial future projections

Two Quicken Classic plans—Premier and Deluxe— require a Windows or Mac desktop download. As you might expect, Classic has more in-depth budgeting, investment tracking, and tax planning features than Empower or Simplifi.

For instance, you can pay bills directly from Quicken Classic and run what-if debt repayment simulations. It also has several personal and small business tax planning tools to prepare Schedule A (itemized tax return), Schedule D (investment income), and other customized tax forms.

Quicken vs. Empower – Syncing Data

Empower and every Quicken tier automatically connects to your banking and investment accounts. You can easily add manual accounts when you want to track the value of a tangible asset or a cash stash, or a financial institution won’t sync.

You can expect daily updates without logging in. Assuming you visit your account multiple times daily, Empower and Quicken connect to your banks at least once every four hours.

As a result, the differences are minute regarding account syncing. You can anticipate seeing your real-time account balances and most recent transactions when logging into either platform. Secondarily, you can exclude duplicate transactions and select categories that might skew your income and expense calculations.

Free data syncing makes Empower one of the best Quicken alternatives when you want to track your spending and investment performance. However, Quicken is better when you must build a robust budget or integrate your transaction data with other money management tools, as mentioned below.

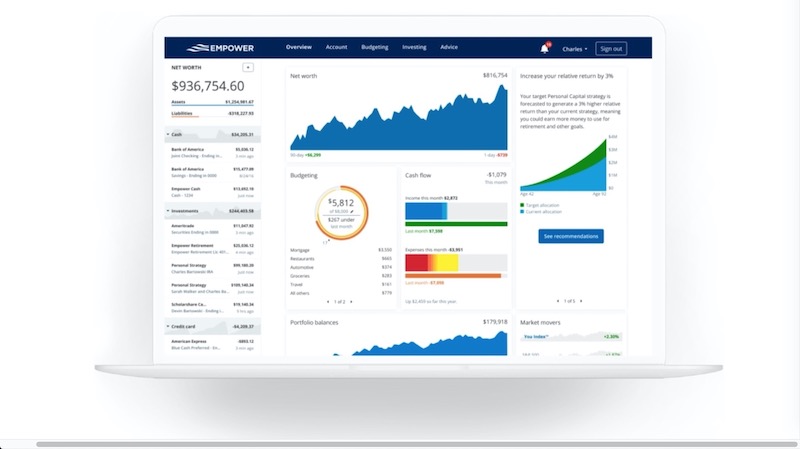

Quicken vs. Empower – Dashboard

Both dashboards highlight various aspects of your finances, such as:

- Budgeting

- Current net worth

- Income and expense history

- Investment performance

- Top expenses by payee

- Synced account balances

Empower is better at tracking your liquid net worth and investment assets as these areas are its specialties. You can view your spending by budget category and compare your actual spending to your planned amount from the dashboard.

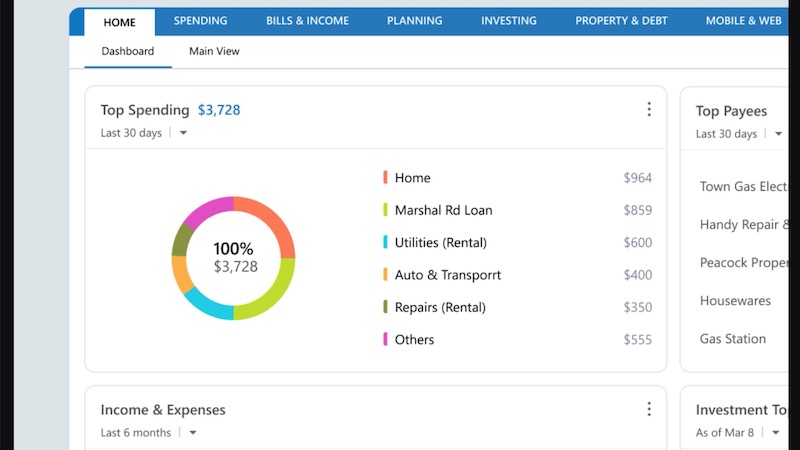

Quicken’s dashboard emphasizes budgeting, bill payment reminders, and spending habits. It also allows you to monitor account balances and individual investment values.

I find each dashboard provides the critical financial details you want to see when logging in. You can then visit multiple menus to gain an in-depth perspective on a specific budgeting, net worth, or investment tracking feature.

I also appreciate the colorful layouts and graphs that make it easier to identify trends and spot unusual transactions.

Quicken vs. Empower – User-Friendliness

Quicken Simplifi and Empower are both easy to use and require minimal setup time. It’s possible to set up either dashboard and start budgeting within an hour through the web platform or mobile app.

The app that works best depends on which features you desire, as each has limitations regarding budgeting, tracking net worth, and investing tools.

For example, I find Empower’s budgeting tools frustrating when you want a category-based budget, or you’re just learning how to manage money. Conversely, Simplifi by Quicken removes the stress from making a hands-on budget and quickly identifies your top expenses by merchant.

However, Empower is suitable to compare my current spending to my planned amounts and account balances since it’s free. It’s also easier to gain an in-depth look at my investment portfolio performance and asset allocation. The net worth calculations can be easier to read and evaluate your future projections.

Quicken Classic is generally the least user-friendly as it’s a desktop platform with the most features. As a result, its setup time can take longer, but you have the most capability to manage your household or business finances.

Quicken vs. Empower – Tracking Investments

You can track your daily and long-term investment performance and compare it to the S&P 500 index with either. In most situations, Empower is the clear winner since it offers several powerful portfolio analysis tools for free with the following features:

- Review your investment performance and allocation with colorful charts

- Estimate future portfolio values at retirement based on Monte Carlo simulations

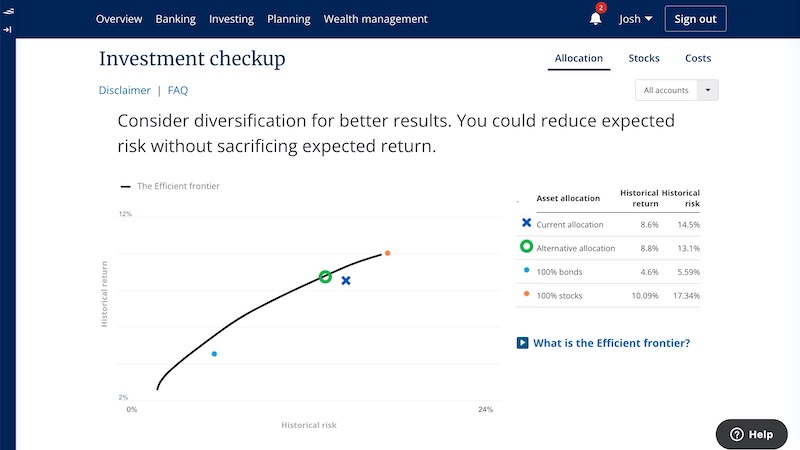

- Compare historical risk and returns for current and alternative allocations

After connecting your brokerage and retirement accounts, Empower performs an investment checkup comparing your current asset allocation to a suggested alternative asset allocation. This analysis may provide more diversification with less risk, allowing you to earn more income over your investing career.

Quicken also has valuable tools for tracking investments that pair well with its budget tools. With Simplifi, you can view real-time quotes and the combined performance of all linked accounts.

I think that Simplifi’s investing tools are great for beginners and users who want to quickly keep track of their various investment accounts in one place.

Serious investors will want the Windows edition of Quicken Classic for exclusive access to these investment optimization tools:

- Customizable views with over 100 fields, including total gain/loss and cost basis

- Estimate capital gains before selling

- Compare the performance of buying or selling to holding positions

- Compare portfolio performance to cost basis, average annual return, and other factors

- Morningstar fund ratings

- Morningstar Portfolio X-Ray

Analyzing your portfolio with Morningstar Portfolio X-Ray lets you review your asset allocation, identify improvement areas, and find your investment strategy’s best strengths. Typically, you must subscribe to Morningstar Investor to procure these insights.

Quicken vs. Empower – Budgeting

With both platforms, you can easily track transactions, savings goals, and actual versus planned spending amounts by budget category. However, Quicken is one of the best budgeting apps with more capable budgeting capabilities overall. I’ll break down the budgeting features into greater detail, as this section can be the most important reason to go with a particular app.

Budgets

Quicken Simplifi can auto-generate a spending plan after analyzing your income and expenses. After the initial assessment, you can customize as necessary and get a “safe to spend” amount that can help avoid overspending when standing in the checkout line.

The desktop versions of Quicken utilize a category-based budget that offers ultimate customization. You can also make multiple budgets, plus fiscal and calendar year business budgets. This version also lets you schedule bill payments from linked bank accounts by check or same-day online payments.

Empower is sufficient to verify your month-to-date cash flow and avoid living paycheck-to-paycheck. You can set your planned spending limit, and the app will tallen your spending. You cannot set category-based limits, but you can tag transactions and recategorize them to improve accuracy as you review your spending patterns.

Regarding budget reports, all Quicken versions are more detailed. Specific examples with Simplifi include custom spending watchlists, spending alerts, built-in spending alerts, and refund trackers.

Savings and Debt Goals

Both platforms let you personalize savings goals and track your progress as you save for upcoming purchases, build an emergency fund, or pay off debt. The better option depends on which budgeting and investment tracking features you need.

Quicken Simplifi lets you incorporate your goals into your monthly budget. You can allocate spending from the savings pod as you withdraw funds and track your debt repayment schedule.

The Empower Savings Planner can suggest how to save money more efficiently. It may recommend boosting your long-term savings, increasing your emergency fund, or paying off debt. You can edit the contribution details and view your financial progress in charts—the platform links to select lenders to retrieve your latest balance and payment history.

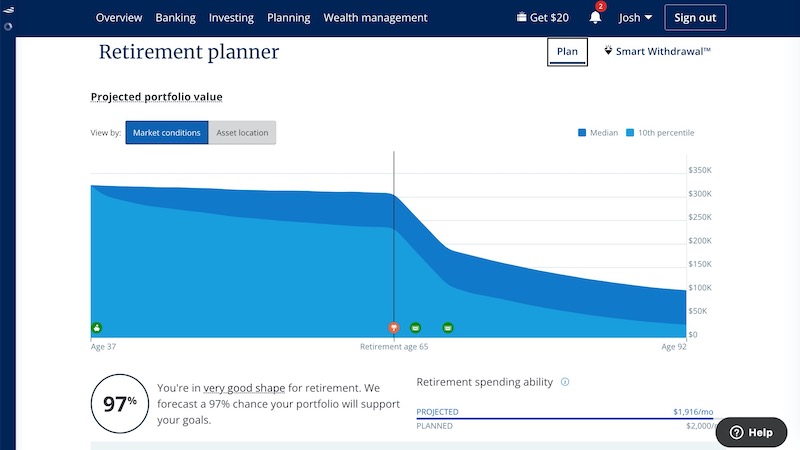

Retirement Planner

A budget or spending plan helps address your short-term finances to ensure you can afford your monthly bills. You can also benefit from a retirement calculator to project how your savings and investments are helping you prepare for later life.

Empower wins this comparison factor with its versatile retirement planning tools. You can project your potential portfolio value during your golden years and the probability of achieving your retirement goals. You can edit select assumptions to fine-tune the projections, although a paid service can be more precise.

Beyond net worth tracking and projections, Quicken’s retirement planning features generally require using the Windows desktop program. This software limitation is frustrating, although the features include what-if scenarios, a lifetime planner, and various financial calculators.

Quicken vs. Empower – Cost

Empower is entirely free, which makes it the most appealing option if you don’t need Quicken’s budgeting tools. You only pay an advisory fee if you enroll in their wealth management services, which include a managed investment portfolio and access to a financial advisor.

My biggest gripe is that an Empower advisor will likely call you when you have at least $100,000 in investment assets. After all, it’s one way the company makes money without selling your data or displaying ads. The initial consultation is free, and there is never an obligation to start investing through Empower to continue using its free financial tools.

Quicken’s pricing varies by plan, and you enjoy up to 25% off with an annual subscription:

- Simplifi: $3.99 monthly or $35.88 billed annually ($2.99 per month)

- Deluxe: $5.99 monthly or $59.64 billed annually ($4.97 per month)

- Premier: $7.99 monthly or $71.88 billed annually (5.99 per month)

Simplifi by Quicken is one of the most affordable budget software with impressive features for its price point. The Deluxe and Premier versions are good, too, when you want extensive money management tools, but you need a Windows operating system for full access.

Quicken vs. Empower – Security

Both Quicken and Empower use bank-level 256-bit encryption to secure your personal data. Two-factor authentication (2FA) and the promise to never sell your data also provide additional reassurance.

Both services also partner with cybersecurity companies and use third-party apps to avoid storing account login details on servers. Desktop Quicken users store their files on their own computer instead of in the cloud as Quicken Simplifi and Empower accounts do.

Empower vs. Quicken Comparison Table

| Empower | Quicken | |

| Budgeting Strategy | Compares monthly actual spending to the planned amount without itemized categories | Income and expense-based for Simplifi/ category-based for Quicken Classic |

| Budgeting Tools | Cash flow tracker, savings planner, debt tracker, bill tracker | Customizable spending plans, safe-to-spend amount, bill tracking and payments, savings goals, debt tracker |

| Account Syncing | Banking and investment accounts | Banking and investment accounts |

| Net Worth Tracker | Tracks linked and manual accounts | Tracks linked and manual accounts |

| Investment Tracker | Links to brokerage and retirement accounts, asset allocation analyzer, retirement fee analyzer | Links to brokerage and retirement accounts, customizable news feeds, capital gains estimator |

| Retirement planning | Retirement calculator, customizable assumptions, personalized suggestions | Projects future account values, lifetime planner (Windows desktop only) |

| Reports and Graphs | Cash flow, investment performance, savings goals, debt repayments, net worth, retirement account projections | Category-based spending reports, top payees, auto-detects bills and subscriptions, spending alerts, refund tracker |

| Accessibility | Web and mobile app | Web and mobile app (desktop-only for Quicken Classic) |

| Customer Service | Email support and chatbot. Advisor access for wealth management clients | Phone, chat, and online community |

| Cost | Free | $2.99 to $7.99 monthly |

Is Empower or Quicken Better?

Empower is ideal if you want a free net worth tracker, basic budgeting, and in-depth investment tracking. It links to most banking and investment accounts which makes it easy to track spending and plan future financial goals automatically. Unfortunately, it’s not great when you need a detailed budget.

Simplifi by Quicken is good for hands-on budgeting, bill reminders, and basic investment tracking. The Quicken Classic desktop versions are best for those wanting an extensive category-based budget and the ability to make multiple spending plans. Its investment tracking and financial planning tools are powerful but Empower may offer similar perks for free.

Frequently Asked Questions

Consider these questions as you compare Empower to Quicken.

Is Quicken free?

Unfortunately, all Quicken plans require a paid subscription, although there’s a 30-day money-back guarantee for a full refund. Its Simplifi web and mobile platform is the most budget-friendly, offering up to 25% savings when purchasing an annual subscription.

Is Empower net worth safe?

Empower (previously Personal Capital) encrypts your information using bank-level security and won’t sell your personal information. Its security guarantee can reimburse losses to your qualifying accounts resulting from unauthorized transactions through no fault of your own.

Does Quicken have a retirement planner?

The Windows desktop version of Quicken Classic includes a lifetime planner feature. Two perks are a personalized retirement plan and a retirement simulator. The entry-level Simplifi plan has minimal retirement planning tools but can project cash flows and track net worth.

Summary

Simplifi gains the winning edge when you want an in-depth budget and the ability to track investment performance, set future goals, and get detailed spending reports. It can be a better fit for beginners wanting hands-on help.

Empower is better when you don’t need a budgeting app and mostly want to track your net worth, see your total monthly spending, and get personalized investing insights. It’s also free, making it worth trying out first to decide if it meets your financial needs.

Source link

")

Q2 2025 earnings")