Over the past couple of weeks and into the next few weeks, you will likely be inundated with economic forecasts and stock market scenarios for 2025. We do not want to add to your pile of scenarios, but we think it may be valuable to share the latest thoughts from our colleague Jim Colquitt of Skillman Grove Research. Jim’s scenarios for 2025 and all of his other research are on his Substack page. Per Jim:

I’m not a big believer in making price forecasts for the upcoming year because as the old Yogi Berra saying goes: “It’s tough to make predictions, especially about the future.”

However, I do think it’s possible to look at the current structure of the market and attempt to decipher some potential scenarios. With that said, I will lay out three scenarios to consider: a) Max Bullish, b) Max Bearish, and c) Somewhere In Between.

Bullish Scenario: The Max Bullish scenario looks at 6,118 and laughs on its way to 7,742 or ~30% higher than Friday’s close. The market never moves in a straight line, so there would be pullbacks along the way, but the ultimate destiny would be somewhere in the neighborhood of 7,742.

Bearish Scenario: Again, markets never move in a straight line, so in this scenario, the market retraces back to the 78.6% Fibonacci (4,050), rallies back a bit, and then has a final flush lower. In this scenario, the target becomes 3,288 or -45% lower from Friday’s close.

In Between Scenario: While the ending target is higher than current prices, you still have to manage a -25% drawdown (5,970 —> 4,488), only to be followed by a 58% increase (4,488 —> 7,096).

What To Watch Today

Earnings

- No earnings releases today.

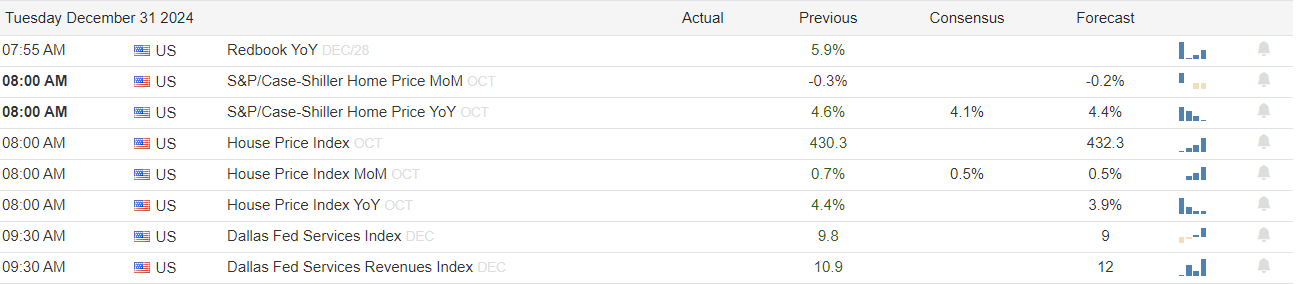

Economy

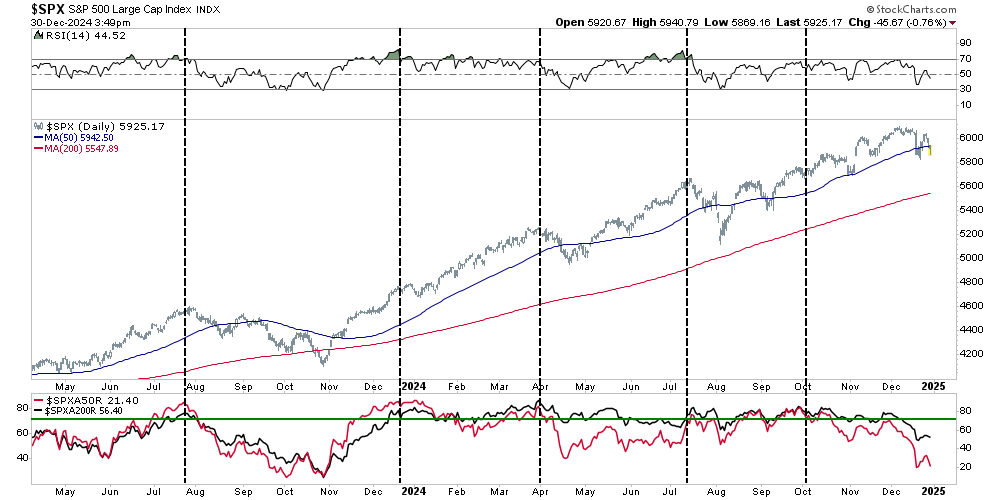

Market Trading Update

As discussed yesterday, Santa Claus may have gotten stuck in the chimney trying to deliver the fabled “rally” into year-end. While there are still three trading days left, time is running short for the market to muster a rally. While breadth has certainly been poor, as shown, selling pressure started early in the day, and markets have rebounded into the day’s end. Such suggests this is likely late portfolio rebalancing and window dressing, but momentum and relative strength remain weak, which raises caution.

While it is still possible for the market to muster a rally into early January (the “Santa Rally” feeds into the first two trading days of January), the overall market action has certainly not been the “joyous occasion” many traders were hoping for. While many headlines are floating around trying to explain the recent weakness, most are just speculation. The rest of this trading week will set the tone for early January, and the inauguration on January 20th will set the tone for the month. Continue to trade accordingly, but if market action doesn’t improve soon, we must revisit portfolios and reevaluate positioning and risk tolerances.

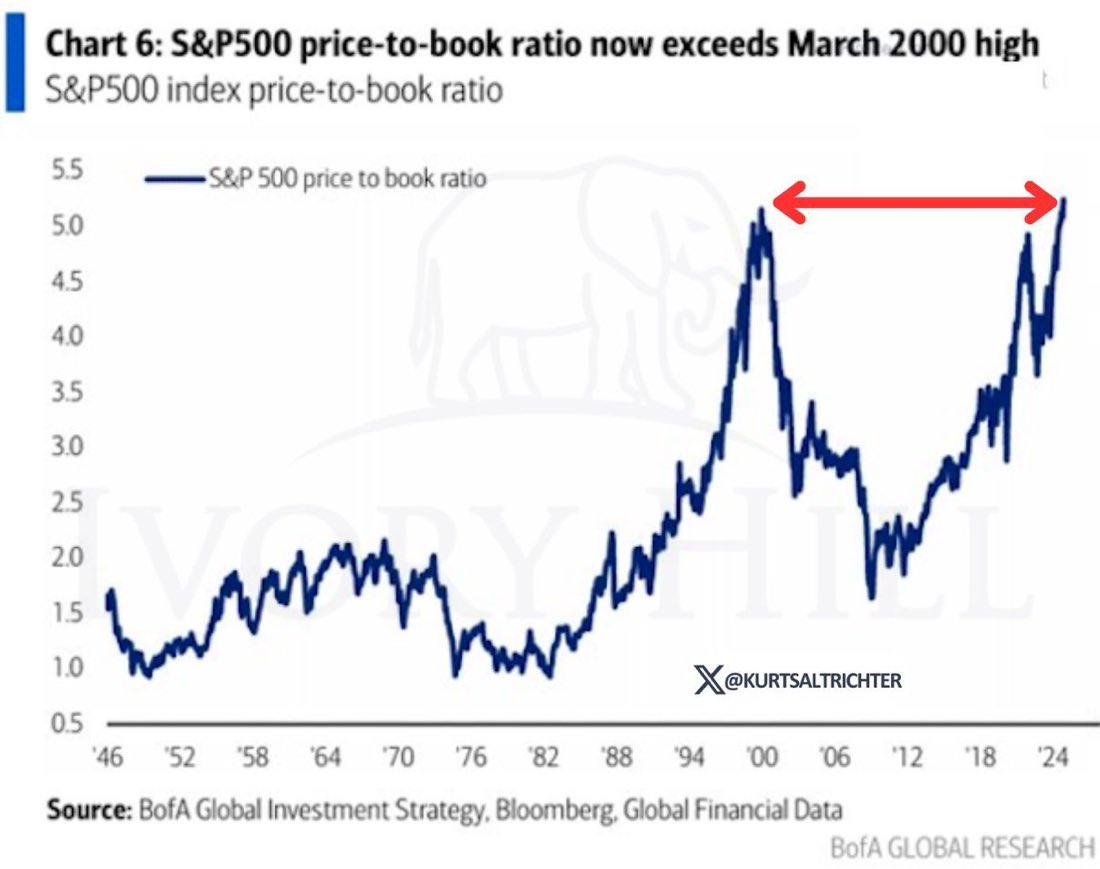

Another Record Valuation

One of our chief concerns for 2025 is a valuation correction. As we have shown numerous times over the year, many stock valuations are near record highs. This denotes that stock prices are rising faster than their fundamentals are growing. The graph below is the latest example of a valuation chart of concern. It shows that the price-to-book ratio of the S&P 500 is now at an 80-year high. Furthermore, it is slightly above the gross overvaluations of 1999.

However, the problem with solely relying on valuations is that they can always get richer before they catch up to reality. For instance, in 1995, investors could have said that the price-to-book ratio of the S&P 500 was too extreme. While they were ultimately accurate, they were five years early. The ratio continued much higher before it significantly corrected. Such may also be the case this time.

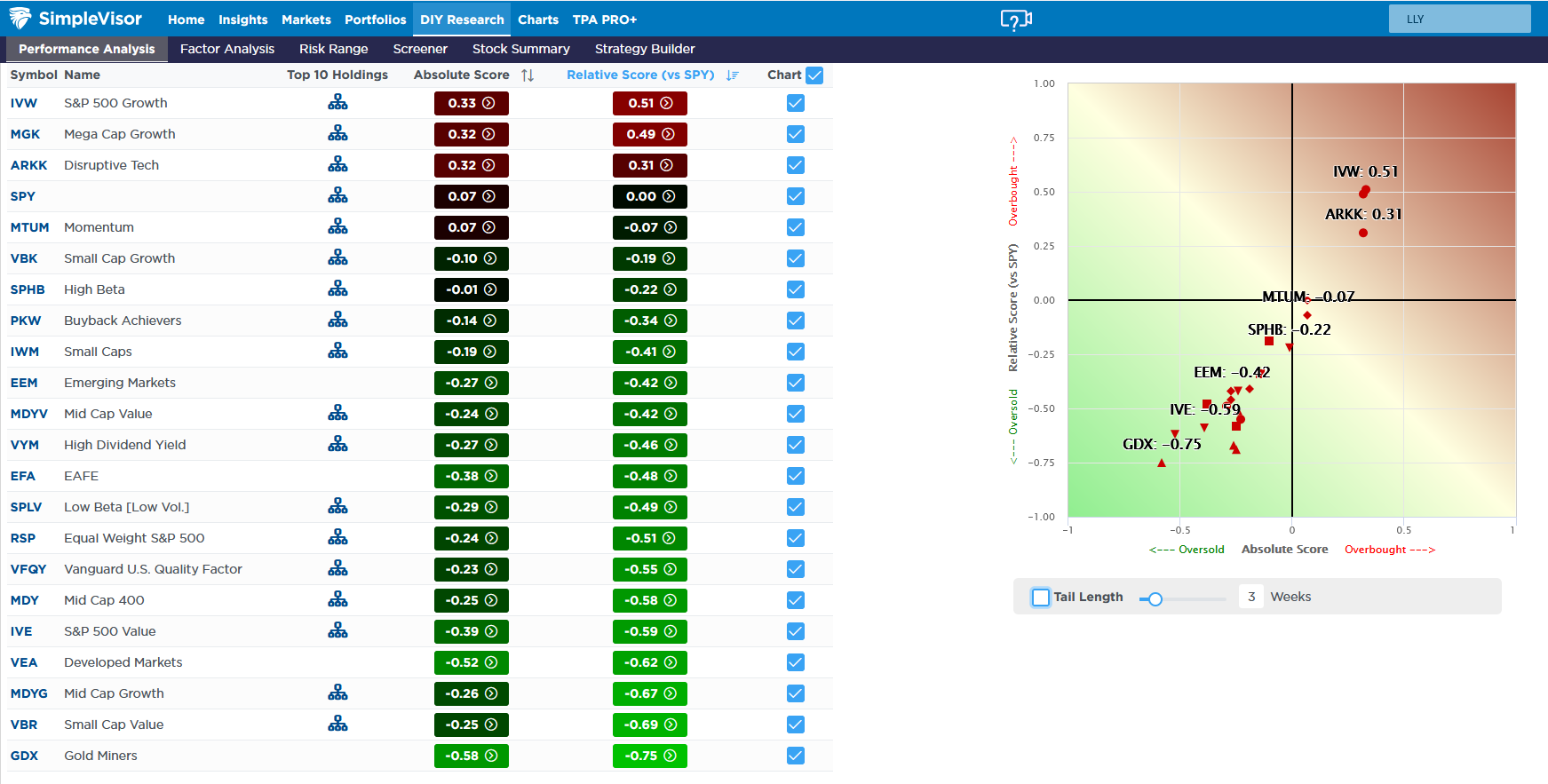

Most Stocks Oversold As Market Meanders

As we share below from SimpleVisor, all stock factors except for large-cap and mega-cap growth and the ARKK ETF are oversold compared to the market. Within those sets, a few big names are leading the charge. For example, the second graphic showing the FINVIZ heat map highlights in green that only a few stocks have been up over the last month, almost all of which are very large-cap stocks. Consider that APPL, AMZN, GOOG, TSLA, and META, the most prominent large-cap gainers, constitute over 20% of the S&P 500.

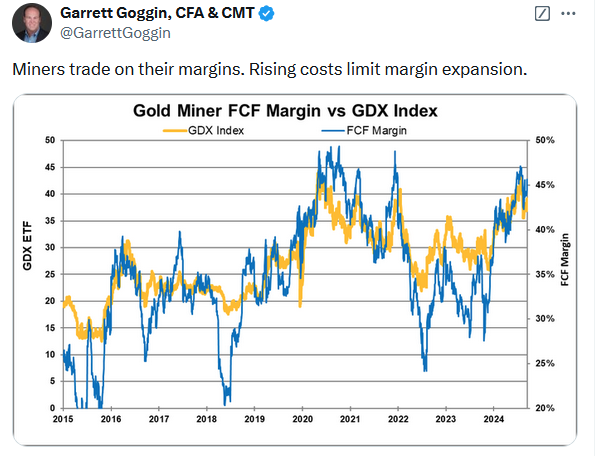

Goldminers are now the most oversold factor from a relative and absolute perspective. Interestingly, as we share in the second graphic, gold miners have performed poorly compared to gold. Over the last weekly and monthly periods, gold was down less than 1%. GDX was down 1% last week and almost 7% over the last month. The top graph shows the ratio of GDX to GLD at its lowest level since April. The technical indicators below the price ratio graph show GDX is on a sell signal versus gold, but those indicators are getting very oversold. GDX may be due for a bounce versus GLD.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Source link