I was emailed several times about a recent Morningstar article about J.P. Morgan’s warning of lower forward returns over the next decade. That was followed up by numerous emails about Goldman Sachs’ recent warnings of 3% annualized returns over the next decade.

While we have previously covered many of these article’s points, a comprehensive analysis is needed. Let’s start with the overall conclusion from JP Morgan’s article:

“The investment bank’s models show the average calendar-year return for the S&P 500 could shrink to 5.7%, roughly half the level since World War II. Millennials and Generation Z might not enjoy the robust returns from U.S. stocks that helped swell the retirement accounts of their parents and grandparents.”

While such a statement may seem obvious to long-time students of markets, the outsized returns over the last decade have many questioning whether “this time is different.” As we discussed in “Portfolio Return Expectations Are Too High.” To wit:

The chart shows the average annual inflation-adjusted total returns (dividends included) since 1928. I used the total return data from Aswath Damodaran, a Stern School of Business professor at New York University. The chart shows that from 1928 to 2023, the market returned 8.45% after inflation. However, after the financial crisis in 2008, returns jumped by nearly four percentage points for the various periods. After over a decade, many investors have become complacent in expecting elevated portfolio returns from the financial markets. However, can those expectations continue to be met in the future?”

After over a decade, many investors have become complacent and now think that these elevated rates of return are “normal.” However, the reality may be quite different.

The stock market is a complex ecosystem with various factors influencing outcomes. Those factors include valuations, inflation, monetary policy, and political regulations. Investors should consider the impact on future stock market returns as we enter a period of potentially higher average inflation (compared to the last decade), less monetary accommodation from central banks, and growing political uncertainty.

Stock Market Valuations: Are We in Bubble Territory?

Valuations are one of the most critical factors in determining future stock market returns. However, valuations are a terrible market timing tool. Valuations only measure when prices are moving faster or slower than earnings. In the short term, valuations are a measure of psychology and the manifestation of the “greater fool theory.“ As shown, there is a high correlation between our composite consumer confidence index and trailing 1-year S&P 500 valuations.

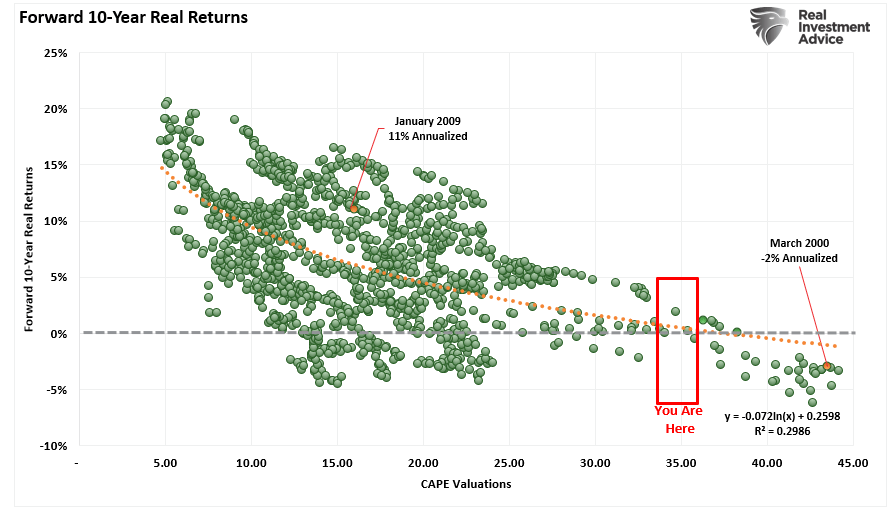

However, where valuations matter is in the long term. Historically, over a decade or more, future returns tend to be lower when stock prices are high relative to earnings. Metrics like the price-to-earnings ratio or P/E ratio often measure such. Conversely, when valuations are low, future returns tend to be higher. The scatterplot chart below compares valuations and returns over a rolling 10-year period.

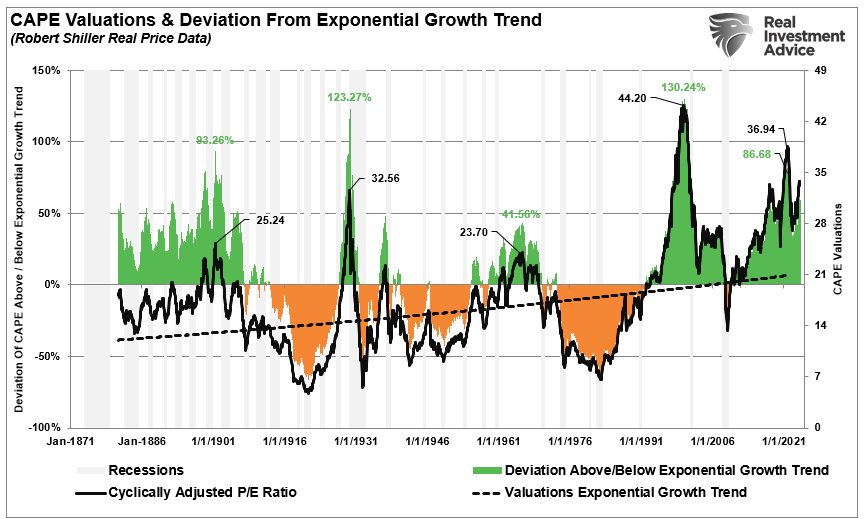

There is little argument that U.S. stock market valuations are elevated compared to historical averages. The S&P 500’s cyclically adjusted price-to-earnings (CAPE) ratio remains well above its long-term exponential growth trend. High valuations reflect optimism but can also signal caution. If the market is pricing in perfection, any disappointment can lead to significant corrections

However, here is the crucial point. High valuations do NOT mean that every year going forward over the next decade will experience a low return. It means the “average” return over the next decade will be low. The chart below shows hypothetical annual market returns with a 10-year average of just 3%. Notice that while 70% of the years provided a return of 10% or more, the 30% of the years with negative returns dragged the average substantially lower. This is the problem of market declines and time.

Inflation also presents another challenge to future returns.

Less Monetary Accommodation: The End of Easy Money?

The Federal Reserve and other central banks worldwide have spent the last decade engaging in highly accommodative monetary policies. Near-zero interest rates and massive asset purchases (known as quantitative easing) provided tailwinds for stock market returns by reducing the cost of borrowing and encouraging risk-taking. However, if inflation settles in at or above the Fed’s 2% target rate, central banks may be forced to pull back on these policies. While the Federal Reserve has been reducing its balance sheet, Government spending (The Inflation Reduction and CHIPs Act) has continued supporting economic growth and earnings.

While the Federal Reserve has started cutting interest rates, it has stated that it does not foresee the Fed Funds rate returning to zero. Therefore, if central banks maintain a higher interest rate environment and continue reducing their balance sheets, reversing “easy-money” conditions may weigh on future returns.

Political and Regulatory Changes

Political uncertainty is another factor that could impact stock market returns. As we look ahead, several potential regulatory changes could influence markets. For instance, increased taxation, stricter environmental regulations, and changes to labor laws could all create headwinds for corporate profits.

One key area of concern is the potential for higher corporate taxes. While the current administration in the U.S. has discussed raising taxes on corporations and high-net-worth individuals, it remains unclear whether such measures will pass through Congress. If corporate tax rates increase, companies may see their after-tax earnings decline, which could put downward pressure on stock prices.

Another area to watch is the regulation of the tech sector. Major technology companies have been under increasing scrutiny by regulators worldwide for issues ranging from privacy concerns to monopolistic practices. Any new regulations aimed at curbing the power of big tech could have significant implications for stock market performance, given the outsized role that technology companies play in today’s market.

This Time Isn’t Likely Different

As stated at the outset, valuations are a terrible market timing metric. However, they tell us much about asset bubbles, investor psychology, and future returns.

No matter how many valuation measures we use, the message remains the same: From current valuation levels, investors’ expected rate of return over the next decade will likely be lower.

There is a large community of individuals who suggest differently and make a case for why this “bull market” can continue for years longer. Unfortunately, no valuation measure supports that claim.

But let me be clear: I am not suggesting the next “financial crisis” is upon us either. I am suggesting that based on various measures, forward returns will be relatively low compared to what we witnessed over the last eight years. Such is particularly the case as the Fed and central banks globally begin to extract themselves from the cycle of interventions.

That statement does not mean that markets will produce single-digit rates of return each year for the next decade. There will be some great years to invest during that period. Unfortunately, most of those years will be spent making up for the losses from the coming recession and market correction.

Conclusion

That is the nature of investing in the markets. There will be fantastic bull market runs, as we have witnessed over the last decade, but to experience the ups, you will have to deal with the eventual downs. This is part of the full market cycles that make up every economic and business cycle.

Despite the hopes of many, no one can repeal the cycles of the market and the economy. While artificial interventions can delay and extend the cycles, the reversion will eventually come.

No. “This time is not different,” and in the end, many investors will once again be reminded of this simple fact:

“The price you pay today for any investment determines the value you will receive tomorrow.”

Unfortunately, those reminders tend to come in the most brutal of manners.

If you want to learn more about how to position your portfolio for the future or seek personalized investment advice, contact our team at RIA Advisors. Schedule a free consultation, and let’s discuss how we can help you meet your financial goals, even in this changing market environment.

Post Views: 2,288

2024/10/25